Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

Global markets sell off majorly. Oil returns to pre-war levels, and gold falls below critical marks

Abstract:Key TakeawaysOil prices fell back to pre-war levels as progress in the U.S.-Iran peace deal eased concerns over supply disruptions and improved the global supply outlook.Gold dropped below $4,000 for

Key Takeaways

Oil prices fell back to pre-war levels as progress in the U.S.-Iran peace deal eased concerns over supply disruptions and improved the global supply outlook.

Gold dropped below $4,000 for the first time since November 2025 after last weeks hawkish Federal Reserve meeting strengthened the U.S. dollar and Treasury yields.

The U.S. PCE inflation report showed prices continuing to rise, but the data came in largely in line with expectations, reinforcing the Feds cautious stance on interest rates.

Global stock markets ended the week lower, with U.S. and Asian equities pressured by expectations that interest rates will remain higher for longer.

Micron Technology surged after beating earnings expectations, as strong demand for AI-related memory chips highlighted the resilience of the AI investment theme.

Oil Retreats as Geopolitical Fears Fade

Oil prices extended their decline throughout the week, giving back nearly all of the gains made during the recent conflict. The continued progress in negotiations between the United States and Iran reduced fears of supply disruptions, while expectations that Iranian crude could gradually return to global markets further improved the supply outlook.

Both WTI and Brent crude fell back to levels seen before the conflict, easing inflation concerns across global markets. Crude brent fell 9% during the week to reach $74. WTI lost nearly 10% to end the week around the $70 level. Markets are increasingly pricing in lower geopolitical risk and a more balanced oil market.

Gold Falls Below $4,000

Gold experienced another difficult week, dropping below the psychologically important $4,000 level for the first time since November 2025. The selloff was largely driven by last weeks Federal Reserve meeting, where policymakers signaled that interest rates are likely to remain higher for longer. Higher Treasury yields and a stronger U.S. dollar reduced the appeal of non-yielding assets such as gold, leading investors to continue taking profits after months of record highs. Silver faced a tough week as well, losing 12% to $57 an ounce. Currently, the Fed, not geopolitics, is the dominant driver of gold prices.

Inflation Readings in Line with Expectation

Thursday's release of the Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve‘s preferred inflation measure, showed that inflation continued to rise. However, the figures came in largely in line with market expectations, avoiding a major surprise for investors. Although the data did not significantly alter expectations for monetary policy, it reinforced the view that inflation remains persistent and supports the Fed’s cautious stance on interest rates. Inflation is proving sticky, reducing the likelihood of rate cuts in the near term.

Stocks End the Week Lower

Equity markets struggled globally as investors continued to digest the Feds hawkish outlook. U.S. indices finished the week lower, with technology stocks remaining under pressure from higher bond yields. Asian markets also weakened as investors reassessed global growth expectations and tighter financial conditions.

One of the weeks biggest winners was Micron Technology. The semiconductor company reported earnings that comfortably exceeded analyst expectations, driven by exceptionally strong demand for AI-related memory chips. Its optimistic outlook sent shares sharply higher and reinforced confidence that AI-related spending remains one of the strongest themes in global markets despite the broader market weakness. AI demand continues to support semiconductor earnings even as the broader market softens.

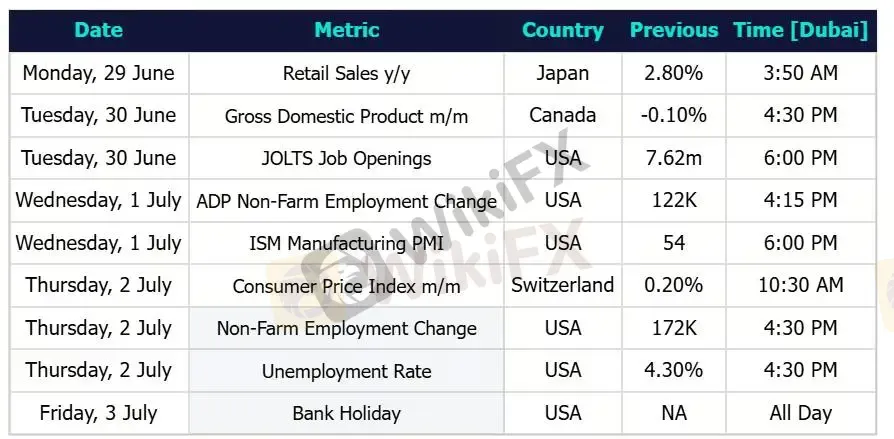

Key Economic Data of the week

The market‘s attention now shifts to a series of employment reports, culminating in next week’s U.S. jobs data. Strong employment data could reinforce expectations that the Federal Reserve will keep interest rates elevated for longer.

Markets will continue monitoring developments surrounding the peace agreement. Any confirmation regarding sanctions relief, Iranian oil exports, or the reopening of key energy routes could continue influencing oil prices and broader market sentiment.

This week marked a clear shift in market focus. While geopolitical risks eased significantly with progress toward a U.S.-Iran peace agreement, investors became increasingly concerned about the Federal Reserve‘s commitment to keeping interest rates higher for longer. The result was lower oil prices, continued weakness in gold, and broad selling across global equity markets. Next week, attention turns squarely to the U.S. labor market, where employment data could determine whether the Fed’s hawkish stance becomes even more firmly entrenched.

Major Economic Calendar Events for the Upcoming Week

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Review 2026: Deriv Regulation, Complaints, and Withdrawal Risk Signals

WikiFX

WikiFXStop Trading in the Middle of Ranging Forex Markets

WikiFXRoboMarkets Review: Regulation Questions Around a Broker Facing Fresh Trading Complaints

WikiFXSTONE WALL CAPITAL Review 2026: Is This Forex Broker Safe?

WikiFXDSI Exposes Alleged Forex Empire Behind Billion Baht Scam, Money Laundering and Political Connection

WikiFXIUX Review:Before Investing a Single Penny, Read These Jaw-Dropping Deposit & Withdrawal Experiences

WikiFXFXTF Review 2026: Japan FSA Regulation, Platform Access, and Exposure Cases

WikiFXReview 2026: FBS Regulation, Complaints, and Withdrawal Risk Signals

WikiFXFXTF Review 2026: Regulation, Withdrawals, and Scam Allegations

WikiFXIG Review 2026: Is This Forex Broker Safe?

WikiFXCurrency Calculator

USD

CNY

Current Rate:0

Enter amount

USD

Redeemable Amount

CNY

Calculate